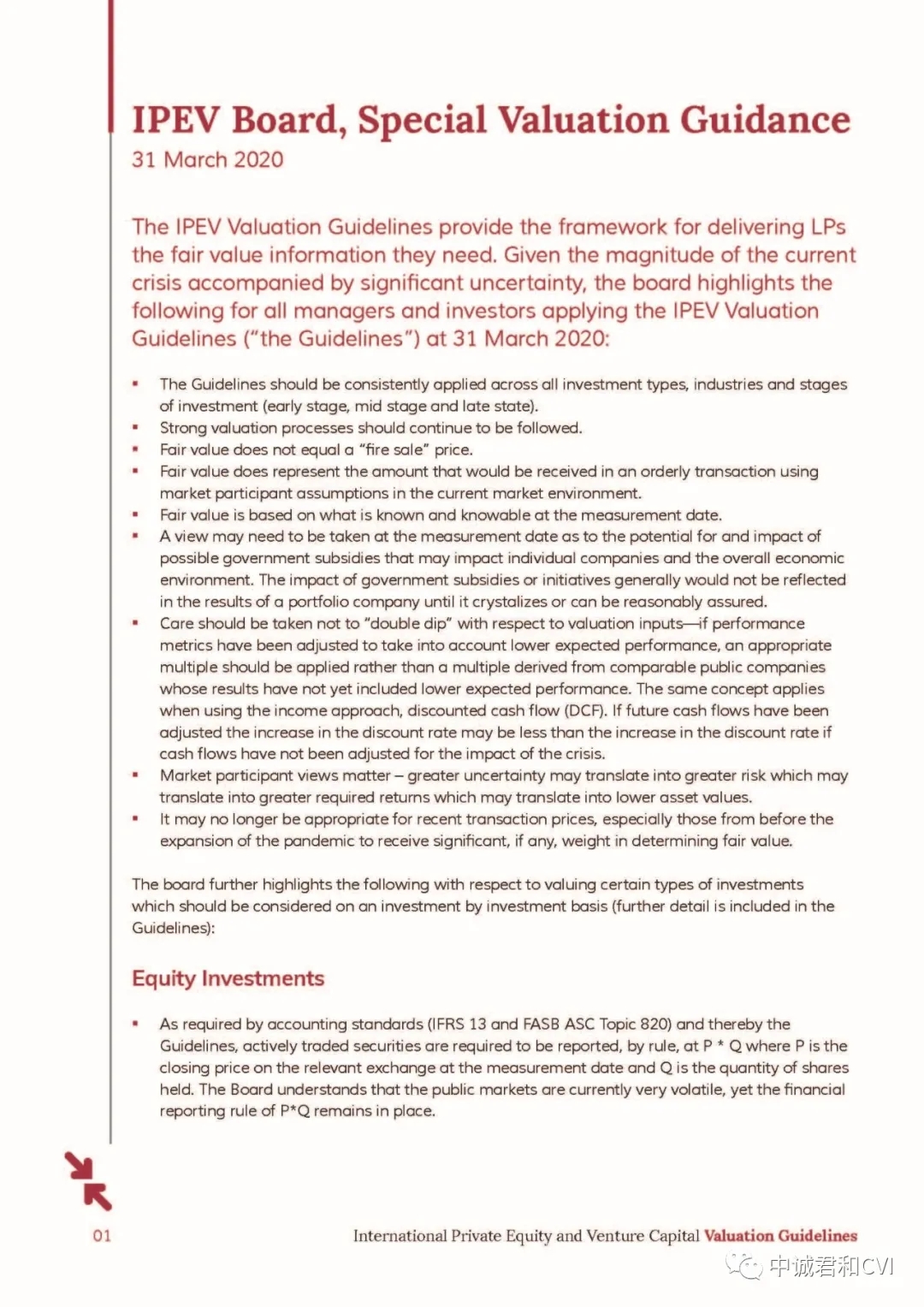

The International Private Equity & Venture CapitalValuation Guidelines Board (“the IPEV Board”) today provides special guidancewith respect to applying the IPEV Valuation Guidelines when estimating fairvalue at 31 March 2020.

TheInternational Private Equity & Venture Capital Valuation Guidelines Board(“the IPEV Board”) 于3月27日发出新闻稿,针对新冠疫情恶化和相关市场的剧烈震荡,对私募股权和风险投资估值在一季度末的公允价值估值提出相关建议。

IPEV Board指出本次危机不同于2001-2002及2008-2009年的危机,已经影响更多的人、业务,影响的速度也更为迅捷;强调需要给投资者提供关于相关投资经营和财务状况的及时的、有用的信息;指出各基金的有限合伙人(LPs)在3月31日时点需要基金经理(GPs)以及时、一致、明确的方式披露相关投资的公允价值。

在2008年危机期间,IPEVBoard指出“公允价值是对私募基金所持有的PE组合公司及投资的最好计量方式”,并在现在的时点再次重申这一原则。2020年3月31日对公允价值的判断将具有极大的挑战性,IVPEBoard紧急制定了《IPEV委员会-特别估值指南-2020年3月31日》(IPEVBoard, Special Valuation Guidance-- 31 March 2020),用于指导一季度末的相关估值。

该估值特别指南的部分内容摘录如下:

@应当继续执行严格的估值程序,Strongvaluation processes should continue to be followed.;

@公允价值不等于“着火价格”,Fairvalue does not equal a “fire sale” price;

@公允价值应当反映现有市场环境下在有序交易中采用市场参与者的假设所能实现的价值数额,Fair value does represent the amount that would be receivedin an orderly transaction using market participant assumptions in the currentmarket environment.

@公允价值应当基于计量日已知和能够知晓的(信息),Fairvalue is based on what is known and knowable at the measurement date;

@在计量日可能会需要考虑政府可能采取的救助行为的影响,如果该救助能够影响企业个体及总结经济与环境。除非政府救助能够具体化或能够合理的确信,否则在相关公司的价值结论中不应当予以考虑。A view may need to be taken at the measurement date as to the potential for andimpact of possible government subsidies that may impact individual companiesand the overall economic environment. The impact of government subsidies orinitiatives generally would not be reflected in the results of a portfoliocompany until it or can be reasonablyassured.

@应当注意在估值参数选取中避免“双重考虑”----如果业绩指标已经反映了恶化的业绩,应当采用适当的倍数,而不能简单采用尚未反映业绩恶化的可比上市公司的倍数。该原则同样适用于收益法(DCF)估值。如果未来现金流已经进行了调整,折现率的上调幅度应当小于未考虑危机因素、未对业绩预测进行调整情况下的上调幅度。Careshould be taken not to “double dip” with respect to valuation inputs—ifperformance metrics have been adjusted to take into account lower expectedperformance, an appropriate multiple should be applied rather than a multiplederived from comparable public companies whose results have not yet includedlower expected performance. The same concept applies when using the incomeapproach, discounted cash flow (DCF). If future cash flows have been adjustedthe increase in the discount rate may be less than the increase in the discountrate if cash flows have not been adjusted for the impact of the crisis.

@在计量公允价值时,近期特别是疫情恶化前的交易价格不应当给予重要权重(或不应当给予权重),Itmay no longer be appropriate for recent transaction prices, especially thosefrom before the expansion of the pandemic to receive significant, if any, weightin determining fair value。

特别指南全文如下:

加载中...

加载中...